Find Your Gold Standard: How to Write a Mission Statement That Shines

Starting a business can feel like digging for gold. Your idea may be strong, but without direction, you risk wasting time and resources.

Your mission statement is not just words — it’s your business’s gold standard, shaping culture, guiding decisions, and protecting your reputation.

Key Takeaways

A mission statement is your business’s compass, guiding decisions and culture.

It must be clear, concise, authentic, and legally accurate.

Avoid misleading claims — under the Australian Consumer Law, false statements risk penalties.

Embed your mission in your business plan, staff handbook, and marketing, and review it regularly.

A strong mission attracts customers, inspires teams, and sets the gold standard for your startup.

What is a Mission Statement?

A mission statement is a short, clear statement that explains:

What your business does

Who it serves

How it delivers value

It is present-focused, unlike a vision statement which describes future aspirations.

Why a Mission Statement Matters

Mission statements clarify what you do, who you serve, and what makes you unique. Business Victoria explains that mission statements focus on present actions, while vision statements outline future goals.

Legal experts warn that what you say publicly matters. Sprintlaw notes that a mission must be authentic, because misleading claims (such as “100% local” without evidence) can expose businesses to legal risk. The ACCC reinforces that under the Australian Consumer Law (ACL), businesses cannot make false or misleading claims.

The Gold-Standard Qualities of a Strong Mission Statement

A strong mission statement should be:

Present-focused and clear – explain what you do now, not vague ideals.

Concise and memorable – usually one sentence, no more than two.

Authentic and compliant – every claim must be accurate and verifiable under Australian law.

Values-driven – show what matters to you and how you act.

Audience-centred – highlight who you serve and what makes you different.

The best mission statements summarise “who, what, why” in a short, simple sentence.

Steps to Create Your Mission Statement

Think of these as your gold-mining tools:

Clarify your “why” and values Reflect on why you started, what you believe in, and the difference you want to make.

Define what you do, and for whom Be specific. For example: “We provide handmade bikes for families in Melbourne” is clearer than “We sell bikes.”

Decide how you deliver value What makes your approach unique? Speed, craftsmanship, sustainability, or innovation?

Draft, simplify, and test Write a rough version, then refine it. Test it with customers, mentors, or your team. Ask: is it clear and believable?

Check compliance Ensure your statement is truthful and not misleading. The ACCC stresses that false claims can breach ACL.

Embed and review regularly Use your mission in business plans, staff handbooks, and websites. Business Victoria recommends reviewing whenever strategy or market conditions change.

Examples of Mission Statements That Shine

Here are two mission statements adapted for Australian startups:

Happy Spokes Bicycles Mission: We handcraft quality, sustainable bikes at affordable prices to help families live healthier, more sustainable lives.

Creative Spark Agency Mission: We deliver tailored design solutions using fresh ideas and innovative tools to help small businesses grow.

Both are short, clear, values-driven, and authentic.

Common Mistakes to Avoid

Even experienced prospectors make mistakes. Watch out for these traps:

Being too vague – e.g., “We exist to change the world” says little.

Mixing mission with vision – mission is present; vision is future.

Making unverifiable claims – e.g., “100% green” without proof risks breaching ACL.

Cramming too much in – keep it simple and memorable.

Letting it gather dust – a mission unused in daily decisions loses its shine.

Expert Insight: “A mission statement must reflect your business’s current reality—what you do, for whom, and how you do it. Otherwise, it risks becoming hollow words.”

Turn Your Mission Into Gold

Your mission statement is your foundation. It inspires your team, attracts customers, and keeps your startup on the right track. Without it, you may dig in the wrong places and miss the gold beneath your feet.

Ready to craft a mission statement that shines like pure gold? DJ Grigg Financial can help you define your purpose, sharpen your message, and embed it in your business.

Striking Gold: How to Define Your Startup Idea with Clarity, Confidence & Viability

Think of your business idea like raw gold. On its own, it’s unrefined and hidden. With the right tools and process, you can mine it, polish it, and reveal its true value.

Key Takeaways

A well-defined business idea improves your chance of long-term success.

Researching your market, competitors, and customers is critical.

Testing, validating, and planning reduce risk.

Understanding legal and financial obligations is essential.

A business plan is your roadmap to growth.

Starting a business is exciting. That first spark—the Eureka! moment—feels electric. But without clarity, a great idea can quickly lose its shine. In fact, according to the Australian Bureau of Statistics, only around 77% of new businesses survive their first year, and just 52% are still operating after four years. The difference between success and failure often comes down to how well you define, refine, and validate your idea.

Why Defining Your Idea Matters

A well-defined business idea gives you:

Direction & focus – a clear path for your decisions and growth.

Confidence – so you can pitch to investors, banks, or partners with clarity.

Customer connection – helping you attract and serve the right people.

As business.gov.au points out, starting a business takes more than passion. You’ll also need the right skills, funding, resilience, and realistic expectations to succeed.

8 Steps to Refine & Validate Your Business Idea

1. Check if You’re Ready

Launching a business is demanding. Ask yourself:

Do I have the time and energy to commit?

Am I financially prepared if profit doesn’t come immediately?

Not every passion project is a business. According to business.gov.au, the key difference is intent to make a profit. Even if you’re not making money yet, if you believe your idea can be profitable, it’s a business—and you’ll need to think about tax, insurance, and compliance.

3. Choose the Right Business Structure

Your business structure affects:

How much tax you pay

Your personal liability

Costs and reporting obligations

Common structures in Australia include: sole trader, partnership, company, trust, and cooperative . Choose carefully—this decision shapes your long-term direction.

4. Research Your Market Thoroughly

Do your homework:

Identify the problem your product/service solves.

Understand your customers—their needs, values, and challenges.

Know your competitors—their pricing, service quality, and unique selling points. The goal? To carve out your own space in the market where you stand out.

5. Validate Your Concept

Talk to potential customers. Test prototypes, offer trial services, and gather feedback. The most important question: Will people actually pay for this?

Expert Insight: “Starting a business without defining your idea is like setting off for gold with a blindfold on. You might stumble on something, but you’ll likely not recognise its value.”

Turning Raw Ideas into Golden Opportunities

Defining your idea is about more than just inspiration. By combining passion with planning, research, and financial insight, you give your business its best chance of not only surviving but thriving.

At DJ Grigg Financial, we help founders test and refine their business models, build strong financial foundations, and set achievable growth goals.

Contact us today to start shaping your business idea into something golden.

Next in our New Business Startups Series: Discover how to craft a mission statement that gives your business true purpose and direction — the guiding compass for your golden journey.

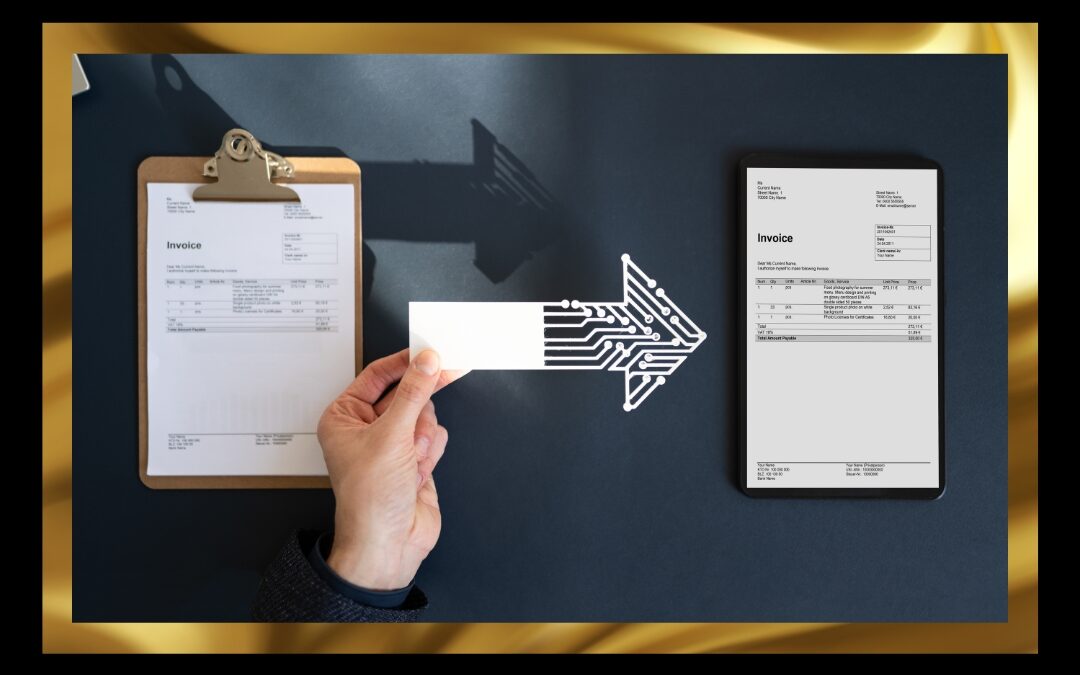

E-Invoicing: The Golden Key to Protecting Your Business from Fraud and Unlocking Faster Payments

In business, protecting your hard-earned income is as valuable as guarding gold in a vault. Traditional invoices can leave you exposed to fraud and cash flow delays. E-invoicing offers a secure, efficient solution—keeping your business safe while helping you get paid faster.

The Risk of Traditional Invoicing

Paper and PDF invoices may look secure, but they are open to manipulation. Invoice redirection scams are one of the fastest-growing threats. The Australian Competition and Consumer Commission (ACCC) reported that Australian businesses lost more than $224 million to payment redirection scams in 2022, with small businesses making up a large share of the victims (ATO).

Scammers often intercept emailed invoices, changing the bank account details before passing them on. By the time the fraud is uncovered, the money is usually gone.

As ACCC Deputy Chair Delia Rickard warns: “Scammers are becoming more sophisticated every year, making traditional invoicing methods more vulnerable than ever.”

E-Invoicing: Your Golden Shield

E-invoicing sends invoices directly between accounting systems using the secure, government-backed Peppol network. This system removes the need for emails or attachments, leaving no opportunity for scammers to intercept or alter invoices.

The ATO, which oversees Australia’s role as a Peppol Authority, explains that e-invoicing allows invoices to “be delivered directly and securely into a business’s software, reducing errors and fraud” (ATO). Importantly, the ATO does not see your invoice data—privacy remains strictly between you, your supplier, and your client.

Think of it as replacing an unguarded gold shipment with an armoured vault that travels straight to your customer.

Faster Payments, Stronger Cash Flow

Security is only half the story. E-invoicing is also a golden ticket to faster payments. Since 1 July 2022, all Australian Government agencies are required to pay Peppol e-invoices within five days, regardless of invoice value (ATO).

That means smoother, more predictable cash flow for businesses that adopt e-invoicing. By reducing processing delays, you can spend less time chasing invoices and more time growing your business.

Cost Savings and Efficiency Gains

Traditional invoice processing costs around $30 per invoice, while an e-invoice can cost under $10. For a business issuing hundreds of invoices each month, the savings quickly add up to a small fortune.

Less manual entry also means fewer errors and disputes, freeing up time for you and your team. In other words, e-invoicing turns invoicing from a time-consuming chore into a streamlined, reliable process.

A Sustainable Choice

Beyond financial benefits, e-invoicing helps businesses reduce their environmental footprint. By cutting down on paper, printing, and postage, it supports sustainability goals while trimming costs. It’s a simple way to make your business practices shine greener as well as gold.

The Right Time to Act

The Australian Government is encouraging businesses of all sizes to adopt e-invoicing as part of its Digital Economy Strategy. More organisations are moving across, and those who delay risk being left behind.

As ATO Assistant Commissioner Emma Rosenzweig puts it: “The sooner businesses make the move to e-invoicing, the sooner they reduce the risk of fraud and errors.”

It’s also worth noting the distinction between invoice redirection fraud (where scammers intercept or alter invoices) and false invoicing schemes (where fake invoices are issued to fraudulently claim GST or deductions). While the ATO’s Serious Financial Crime Taskforce focuses on stamping out false invoicing fraud, e-invoicing primarily protects your business against interception and redirection scams (ATO).

Unlock the Golden Advantage

E-invoicing is not just a digital upgrade—it’s a powerful safeguard, a cost saver, and a tool for growth. By adopting it now, you protect your business, improve your cash flow, and future-proof your operations.

Contact DJ Grigg Financial today to set up e-invoicing and give your business the golden advantage.

How to Improve Your Procurement Spending: Turn Costs into Gold

Procurement is one of the largest expenses for most businesses. Whether you’re buying materials, services, or technology, the way you manage these costs directly impacts profitability. Without proper oversight, money can drain away like gold dust slipping through your fingers.

So how do you transform procurement spending into a source of savings and long-term business value? Let’s explore practical, proven strategies that align with Australian Taxation Office (ATO) guidance and broader procurement best practice.

Why Smarter Procurement Matters

Most businesses underestimate the impact of procurement on their bottom line. From supplier contracts to freight costs, procurement touches every part of operations.

According to Deloitte’s 2023 Global Chief Procurement Officer Survey, nearly 80% of business leaders see procurement as vital to growth and resilience. However, many fail to optimise it strategically.

“Procurement isn’t just about cutting costs—it’s about building value,” says Sarah Jameson, supply chain consultant at Proxima. “With smart strategies, companies can achieve 10–15% annual savings and strengthen their supplier networks”.

Five Golden Rules to Improve Procurement Spending

Think of procurement like panning for gold. With patience and the right tools, you uncover valuable opportunities hidden beneath the surface.

1. Reduce Your Base Cost Per Item

The cost per unit is the foundation of procurement spending. Even small reductions shine brightly across your financial results. Get multiple supplier quotes, benchmark pricing, and negotiate firmly for value, not just the lowest price. Regular reviews can help ensure you’re still getting the best deal.

Tax Tip: Procurement expenses that are directly related to earning assessable income are generally deductible, as long as you keep records (ATO).

2. Cut Your Logistics and Delivery Costs

Freight and delivery can quietly erode margins. Regularly review your logistics providers and explore discounts for early payment or preferred-customer arrangements. A long-term commitment often brings stronger partnerships and better prices.

Like polishing gold, reducing logistics expenses reveals hidden value you may be overlooking.

3. Build Strong Supplier Relationships

Trust and collaboration are worth more than gold in procurement. Pay suppliers on time, communicate openly, and treat them as partners. This goodwill can deliver flexibility, reliability, and better terms.

“Healthy supplier relationships create resilience that short-term cost-cutting cannot match,” says procurement expert John Riley, quoted in Supply Management Magazine.

Government procurement guidance also highlights that value-for-money is achieved through both price and the quality of supplier relationships (Australian Government Procurement Framework).

4. Reduce Tax and Duty Costs

Hidden costs often appear in taxes and import duties. Working with a tax adviser ensures you are only paying what is necessary, while a customs broker can streamline international shipping processes.

The ATO stresses that deductions are available only where expenses are properly documented and directly tied to income generation (ATO – Business Deductions). Engaging experts helps you stay compliant while protecting your cash flow.

5. Use Technology to Take Control

Procurement software gives businesses real-time visibility over spending, budgets, and supplier performance. Cloud-based systems help identify overspending, manage risks, and automate reporting.

McKinsey estimates that companies using digital procurement tools can cut costs by up to 20% (McKinsey).

ATO Perspective: While the ATO doesn’t endorse specific software, it requires reliable and accessible record-keeping for all deductible expenses (ATO – Record Keeping). Digital procurement tools help businesses stay compliant while gaining financial insight.

Strike Gold with Smarter Procurement

Improving procurement is not about penny-pinching—it’s about strategic control. By refining processes, negotiating effectively, and leveraging technology, businesses can strike gold in their finances.

At DJ Grigg Financial, we help businesses uncover savings, strengthen supplier relationships, and ensure their procurement practices support both compliance and profitability.

Ready to turn procurement costs into golden opportunities? Contact us today and let’s unlock the value hidden in your spending.

Are You Suffering from Business Burnout? Golden Tips for Self-care

Running a business often feels like spinning plates—clients, staff, cash flow, family, and late-night admin. But when you forget to look after yourself, the whole show can come crashing down. This July 25 was International Self-Care Day. It was the perfect reminder that self-care isn’t a luxury—it’s a lifeline that matters for a lifetime.

Why Self-Care Matters More Than Ever

Research shows small business owners are under pressure. 56% report experiencing anxiety or depression, and 43% worked every weekend prior to the pandemic (Business Victoria). Meanwhile, 77% of sole traders feel isolated, with 59% describing themselves as mentally and physically exhausted (News.com.au).

As mental health advocate Dr Matt Agnew puts it:

“Without structured work patterns in place, it’s very easy to slip into working an unsustainable amount of hours.” (News.com.au)

Think of your wellbeing like your business finances: you wouldn’t wait until your bank account hit zero before taking action. The same golden rule applies to your health—invest early and consistently.

Spotting the Warning Signs of Burnout

Burnout is like rust—it creeps in slowly until the shine is gone. Key signs include:

Physical: fatigue, poor sleep, headaches or digestive issues

Emotional: feeling anxious, overwhelmed or sad

Behavioural: irritability, low motivation or increased reliance on alcohol

Social or financial pressures: juggling debt, isolation, or constant multitasking

Left untreated, burnout may lead to long-term health issues such as heart disease, insomnia, and type 2 diabetes (Ahead for Business).

Golden Strategies to Recover and Recharge

1. Delegate the Dull

Stop hoarding low-value tasks like bookkeeping or admin. Paying someone else saves energy and frees time for growth.

2. Re-energise Your Purpose

If you’re losing enthusiasm, connect with a mentor, business coach, or peer network. Sharing challenges with others can reignite motivation.

3. Stand Back and Set Boundaries

Review how much you work versus how effective you are. Put golden boundaries around your hours and protect them like treasure.

4. Reassess Your Goals

Are your current goals realistic? Adjusting them to match your energy levels keeps you moving forward without overwhelm.

5. Commit to Daily Self-Care Actions

Build golden habits such as daily walks, balanced meals, or mindfulness apps that remind you to take mini breaks.

6. Celebrate Your Wins

Don’t wait for the “big deal” to celebrate. Recognise milestones, no matter how small. Gratitude is a powerful stress-buster.

Practical Everyday Self-Care Tips

Small actions create lasting results. Try one or two this week:

Structure your day around three main tasks

Take proper meal breaks—nobody thrives when “hangry”

Create a simple self-care plan for consistent wellbeing

Build a trusted support team around you

Join a local business group to share ideas and reduce isolation

Professional Support for Business Owners

Support is always available. Helpful resources include:

These resources can lighten your admin workload and support better self-care.

Final Thoughts: Guard Your Gold

Your business shines brightest when you do. Self-care is the polish that keeps your health, mindset, and resilience gleaming. Don’t wait until burnout dulls your shine—invest in yourself now.

At DJ Grigg Financial, we know that when you’re supported, your business thrives. If you’re ready to delegate, streamline, or get financial clarity, contact us today—we’ll help you protect your most valuable asset: you.