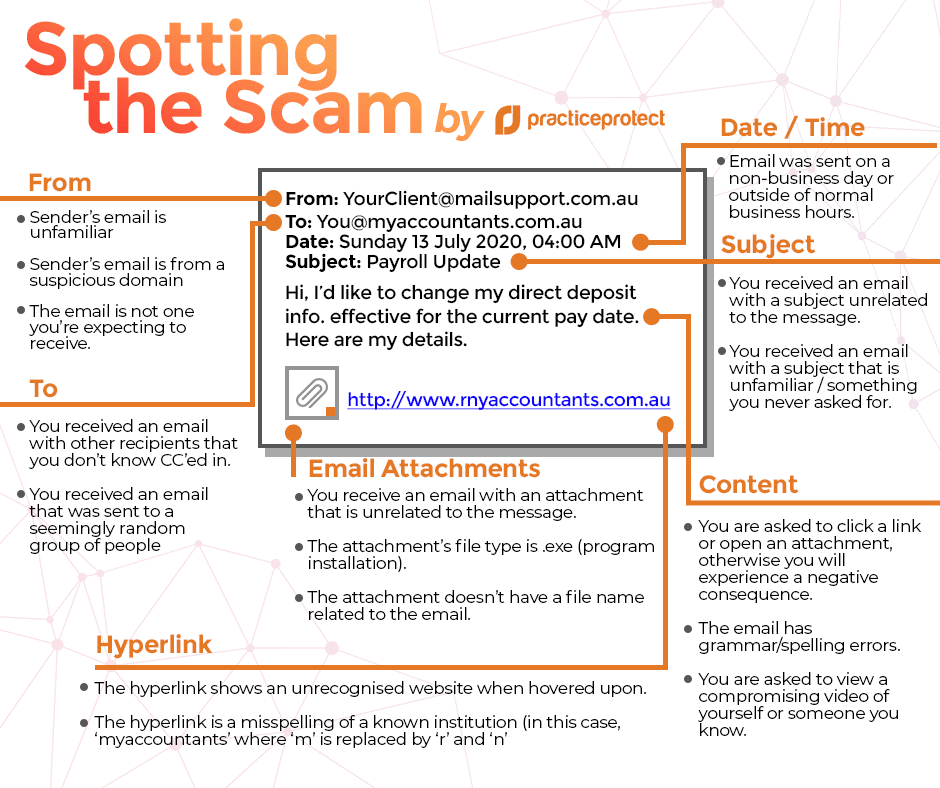

ATO Crackdown: Claiming Working from Home Related Expenses Correctly

With the ATO intensifying its scrutiny on incorrectly claimed work-related expenses, particularly for those working from home, it’s crucial to understand the right way to claim deductions. As tax time 2024 is here, taxpayers must ensure they are accurately identifying and claiming work-related expenses to avoid penalties. This article provides a comprehensive guide on how to navigate these claims correctly, ensuring you stay compliant and maximise your eligible deductions.

Why the ATO is Focusing on Work-Related Expenses

Claiming work-related expenses is an area rife with errors, making it a primary focus for the ATO this tax season. In 2023, more than eight million taxpayers claimed a work-related deduction, with about half relating to working from home costs. The increase in remote work has made understanding the methods for calculating these deductions more critical than ever.

“Copying and pasting your working from home claim from last year may be tempting, but this will likely mean we will be contacting you for a ‘please explain’,” says ATO Assistant Commissioner Rob Thomson. “Your deductions will be disallowed if you’re not eligible or you don’t keep the right records.”

Methods for Calculating Working from Home Expenses

There are two primary methods for calculating work from home expenses: the actual cost method and the fixed rate method. It’s important to choose the one that best suits your situation, as these methods cannot be combined.

Actual Cost Method

This method involves calculating the precise cost of expenses incurred while working from home. This includes costs such as:

– Electricity and gas for heating, cooling, and lighting

– Home office equipment and furniture depreciation

– Internet and phone expenses

To use the actual cost method, you must keep detailed records of all expenses and the portion of these costs that relate directly to your work.

Fixed Rate Method

The fixed rate method allows you to claim a set rate of 67 cents per hour for work from home expenses. This covers:

– Running costs like electricity and gas

– Phone and internet expenses

– Home office equipment depreciation

Like the actual cost method, detailed records of hours worked from home and evidence of expenses are essential.

The ATO’s Three Golden Rules

Regardless of the method you choose, the ATO has three golden rules for claiming work-related expenses:

1. You must have spent the money yourself and not been reimbursed.

2. The expense must be directly related to earning your income.

3. You must have a record to prove the expense.

These rules are designed to ensure that only legitimate work-related expenses are claimed. Failure to adhere to these rules can result in your claim being disallowed.

Eligibility for Claiming Working from Home Expenses

To be eligible to claim working from home expenses, you must meet specific criteria:

– Fulfill Employment Duties: You must be performing your employment duties while working from home, not just minimal tasks like taking calls or checking emails.

– Incur Additional Running Expenses: You should have additional expenses due to working from home, such as increased electricity or gas costs.

– Keep Detailed Records: Maintain detailed records showing how these expenses were incurred and how they relate to your work.

Expert Advice on Claiming Work From Home Expenses

Keep Accurate Records

One of the most common mistakes is failing to keep accurate records. This includes:

– Receipts and invoices for all claimed expenses

– A logbook or diary showing hours worked from home

– Evidence of how you calculated the work-related portion of expenses

PRO TIP: Keeping meticulous records not only ensures compliance but also maximises your eligible deductions.

Choose the Right Method

Selecting the appropriate method for your situation is crucial. The actual cost method can result in higher deductions if you have significant running costs, but it requires more detailed record-keeping. The fixed rate method is simpler but might not capture all your expenses.

PRO TIP: Evaluate your work from home setup and expenses carefully before deciding which method to use.

Avoid Common Pitfalls

Many taxpayers fall into the trap of over-claiming or including non-deductible expenses. Common errors include:

– Claiming the entire internet or phone bill without apportioning the work-related usage

– Including expenses for household members

– Claiming expenses for minimal tasks not directly related to earning income

PRO TIP: It’s easy to overestimate deductions without realising it. Ensure you only claim what is directly related to your work.

Statistics on Work-Related Deductions

The ATO’s increased focus on work-related deductions is backed by significant statistics:

– Over 8 million taxpayers claimed a work-related deduction in 2023.

– 50% of these claims were related to working from home costs.

– Incorrect claims result in millions of dollars in adjustments each year.

These figures highlight the importance of getting your work-related expense claims right. By adhering to the ATO’s guidelines and keeping detailed records, you can avoid the risk of penalties and ensure your deductions are maximised.

Conclusion

As the ATO intensifies its crackdown on incorrectly claimed work-related expenses, especially for those working from home, it’s vital to understand the correct methods for claiming deductions. By following the ATO’s guidelines, keeping accurate records, and choosing the appropriate calculation method, you can navigate tax time with confidence and compliance.

Stay informed, stay diligent, and make sure your work-related expense claims are accurate and justified. Doing so will not only keep you on the right side of the ATO but also ensure you receive the deductions you’re entitled to.

Additional Resources

For more detailed information, see this article, or visit the ATO website where you can find comprehensive guides on claiming work-related expenses, as well as tools and calculators to help you determine the best method for your situation.

Stay Safe This Tax Season: Guard Against Rising Tax Scams

As tax season approaches, business owners and employees alike need to be vigilant against a rising tide of tax time scams. Despite the proactive measures taken by the Australian Taxation Office (ATO) and the National Anti-Scam Centre (NASC), fraudsters continue to find new ways to deceive unsuspecting taxpayers. With a notable increase in ATO impersonation scams reported in recent months, it’s crucial to understand the tactics scammers use and how to protect yourself. This article delves into the prevalent scams, offers expert advice, and provides practical steps to avoid becoming a victim.

The Rise of ATO Impersonation Scams

Recent data indicates a troubling 31% increase in reports of ATO impersonation scams through various channels such as SMS, email, phone, and social media as tax time approaches in 2024. These scams often involve unsolicited contact where fraudsters pose as ATO representatives offering refunds, assistance with tax issues, or alerting taxpayers to suspicious activity on their accounts.

Despite the efforts of the ATO and NASC, which have resulted in over 5,000 fraudulent website takedowns and the blocking of 100 million scam text messages in the last quarter of 2023, scammers continue to evolve their tactics. This persistence underscores the need for heightened awareness and caution during tax season.

Understanding the Tactics of Scammers

Scammers use a variety of methods to trick taxpayers into divulging personal information or transferring money. Some common tactics include:

– Phishing Emails and SMS: These messages often contain links to fake websites designed to steal personal information or install malware. The ATO has responded by removing hyperlinks from all outbound unsolicited SMS to prevent such scams.

– Phone Scams: Scammers might call, posing as ATO officials, and create a sense of urgency, demanding immediate payment to avoid penalties or legal action.

– Social Media Scams: Fraudsters may use social media platforms to contact individuals directly, offering tax refunds or threatening legal consequences.

Real Stories, Real Risks

Consider the case of John, a small business owner who received an email that appeared to be from the ATO, claiming he was due for a significant tax refund. Excited, he clicked the link and entered his personal and financial details. A week later, John discovered his bank account had been drained, and his personal information was used to open fraudulent accounts in his name.

Unfortunately, John’s story is not unique. Many individuals and businesses fall victim to similar scams each year, highlighting the importance of vigilance and education.

Expert Advice: How to Avoid Tax Scams

Be Skeptical of Unsolicited Contact

The ATO emphasises that they will never contact you through unsolicited email, SMS, or social media to ask for personal information or payment. If you receive such a message, do not engage. Instead, look up the ATO’s official contact numbers and verify the communication.

“Always verify unsolicited contact independently. Scammers often create a sense of urgency, but taking a moment to verify can save you from significant losses,” advises Sarah Johnson, cybersecurity expert at SecureNet Solutions.

Check for Authenticity

When in doubt, visit the ATO website directly. The ATO provides detailed information about ongoing scams and how to recognise them. They also offer a reporting service for any suspicious communication.

We’re attaching here, an Infographic put together by our Cybersecurity partner Practice Protect. This infographic highlights how you can spot an email scam.

“Legitimate organisations like the ATO will have secure methods for contacting you. Be wary of any communication that deviates from their standard procedures,” says Mark Harris, a fraud prevention specialist.

Use Strong Cybersecurity Practices

Ensure your devices are protected with up-to-date antivirus software, and be cautious about the information you share online. Regularly update your passwords and use two-factor authentication whenever possible.

“Cybersecurity is an essential layer of defense against scams. Protecting your digital footprint can prevent scammers from accessing sensitive information,” states Emily White, IT security consultant.

Proactive Measures by Authorities

The ATO and related authorities are continually working on new measures to combat scams. The creation of NASC and funding for the Australian Securities and Investments Commission (ASIC) and the Australian Communications and Media Authority (ACMA) to take down fake investment websites are steps in the right direction. The establishment of the SMS Sender ID register to stop scammers from spoofing trusted brand names has also been effective.

In addition, the ATO has a dedicated team monitoring for scams and assisting victims. They offer comprehensive resources and guidelines on their website to help the community recognise and report scams.

Statistics and Success Stories

The efforts of the ATO and NASC have led to significant achievements in scam prevention:

– Over 5,000 fraudulent websites were taken down in the final quarter of 2023.

– More than 100 million scam text messages were blocked during the same period.

– 31% increase in reports of ATO impersonation scams in May 2024 highlights the ongoing battle against scammers.

These statistics underscore the importance of remaining vigilant and the positive impact of coordinated efforts to combat fraud.

Conclusion

Tax time is a critical period for business owners and employees, making it a prime target for scammers. By staying informed about the latest tactics used by fraudsters and following expert advice, you can protect yourself and your business from falling victim to tax time scams. Remember to verify unsolicited contacts, check for authenticity, and practice robust cybersecurity measures. The collective effort of individuals and authorities is key to mitigating the risks posed by these persistent scams.

Understanding the Basics: Business Asset Depreciation

Business asset depreciation is what happens when business assets lose value over time.

It’s an often-forgotten cost of doing business – but it shouldn’t be. Here’s why depreciation is so important:

Costs you money – Depreciation accounting involves calculating how much value your assets lose each year. It can be listed as a loss and subtracted from your revenue.

Can reduce your tax bill – Because depreciation is a business cost, it can lower your tax bill. That’s why it’s important to know how much value you’re losing each year.

Affects the value of your business – If major business assets lose value, the overall value of your business is reduced. Inaccurate tracking could lead to overestimating your business value, making it harder to secure finance.

The ins and outs of business asset depreciation

Usually, only long-term or fixed assets can be depreciated, while consumable products aren’t included.

You also need to estimate the item’s lifespan and choose a method to calculate how its value declines over time.

Common methods include:

Straight line depreciation: the asset depreciates by the same amount each year, eventually reaching zero value.

Diminishing value depreciation: the value declines by a higher percentage in the first few years, then the rate of depreciation slows.

Units of production depreciation: the lifespan is calculated by the value delivered, not the time spent using the asset. For example, a business vehicle’s depreciation might be measured in kilometres travelled rather than age.

Accounting for depreciation in your business

When you’re just starting out, calculating depreciation can seem overwhelmingly complex. But, because it can lower your costs and help you track your business value, it’s worth making the effort.

If you’re not sure where to start, click here to get help from our expert accounting team now.

For more on our ‘Understanding the Basics’ series, see:

When running a business, it’s essential to understand the different types of taxes that apply. Depending on your business structure, you may be required to pay a variety of taxes. The most common taxes include:

Goods and Services Tax (GST)

Income Tax

Pay As You Go (PAYG) Withholding for employees

Payroll Tax

Excise Tax

In addition to these, your business might also encounter:

Fringe Benefits Tax (FBT)

Capital Gains Tax (CGT)

Property Taxes

Vehicle Taxes

State and Local Government Duties and Levies

Taxes Paid on the Business Activity Statement (BAS)

Once your business is registered for applicable taxes, you’ll report and pay many of them through your monthly or quarterly Business Activity Statement (BAS). Key taxes paid via BAS include:

GST: Your business collects GST from customers and pays it to suppliers, then pays the difference between the GST on sales and purchases.

PAYG Withholding: This applies to payments made to employees or suppliers who do not provide an Australian Business Number (ABN).

PAYG Instalments: Contribute towards your expected income tax bill.

Other taxes that may be included on the BAS (if applicable) are:

Fringe Benefits Tax (FBT) instalments

Fuel Tax Credits

Wine Equalisation Tax (WET)

Luxury Car Tax

State Revenue Office Taxes and Fees

Some business taxes are paid directly to your State Revenue Office. These can include:

Land Tax for property purchases

Payroll Tax (once your reportable wages exceed the state threshold)

Stamp Duty on property transfers

Income Tax for Businesses

At the end of the financial year, your business calculates income tax, factoring in any PAYG instalments already paid. By claiming tax deductions for business expenses, you can reduce your taxable income and lower your tax bill.

If your business makes a financial gain from disposing of assets, such as property or shares, you’ll pay Capital Gains Tax (CGT). This tax is part of your overall income tax. Income tax rates and calculations vary depending on your business structure, such as a sole trader, partnership, company, or trust.

Small Business Tax Concessions

If you’re a small business, you may qualify for tax concessions that reduce your tax liability. These concessions can apply to:

Asset write-offs

Primary producers

Fringe benefits

Start-up expenses

Additionally, there are Capital Gains Tax (CGT) concessions available to small businesses that can further reduce the tax payable.

Thinking of Starting or Changing a Business?

Before starting or making changes to your business, it’s crucial to plan for the taxes you’ll need to manage. Speak with a tax agent about adding or cancelling tax registrations, claiming concessions, and staying compliant with tax laws.

For more on our ‘Understanding the Basics’ series, see:

Australian residents pay personal income tax on all forms of income after a tax-free threshold of $18,200. The tax office calculate tax at four different rates according to how much income you earn each year, and the tax rate increases the more you make. The highest tax bracket applies to those with a taxable income of more than $180,001.

ATO taxes foreign residents, children, and working holidaymakers differently.

Income tax is the most significant type of tax the ATO collects, making up around half of all taxes they receive.

Types of Taxable Income

The ATO calculates tax on various forms of income, including employment, government support, investment, and business income.

Employment income includes; wages, salary, allowances, bonus payments, termination payments, some lump sum payments, fringe benefits, and superannuation contributions.

Government support includes all pension payments, allowances, carer support, and COVID-19 support payments. Some government support, such as disaster recovery payments, are tax exempt.

Investment income includes interest paid by financial institutions, share dividends, rent from investment properties, managed investment trusts, and capital gains from profit on selling assets. This also includes cryptocurrency gains.

Business income for sole traders is assessed as personal income, while business income for other entities such as companies is taxed separately to the individuals running the business entity.

Annual Tax Return

You have to declare all types of income, Australian and foreign. Any income received in foreign currency needs to be converted to Australian dollar value.

Most people need to lodge a tax return with the Australian Taxation Office each year by 31 October. If you have a tax agent lodging on your behalf, you’ll get an extension.

Your employer withholds tax from your wages or salary each pay period and pays the ATO on your behalf. If you’ve earned more money from other sources, such as investments or a side hustle, you might end up with a tax bill in addition to what has been withheld from your pay. When we calculate your taxable income, we’ll let you know in plenty of time if you have to pay more.

Make the Most of Allowable Deductions

Allowable deductions vary significantly according to the type of income you have earned. You can’t claim private expenses or anything that an employer has reimbursed.

Common deductions include home office, tools and equipment, accounting fees, donations, personal super contributions, and vehicle expenses. However, it’s best to check with us as you may be able to claim other expenses such as education, cleaning, or professional memberships.

When preparing your tax return, we will include any allowable offsets, rebates, or concessions that may apply to your situation to reduce your tax bill. We’ll also check that you’ve included all allowable deductions for your situation.

Click here to make an appointment with one of our tax accountants.

For more on our ‘Understanding the Basics’ series, see:

A capital gain (or loss) occurs when an asset is sold. The difference between the purchase price and the sale price is the gain or loss. Capital gains tax (CGT) applies to money you have made from selling an eligible asset.

Capital gains tax events occur when an asset is sold, or other triggers arise, such as the loss, theft, or destruction of an asset, or creating contractual or other rights to an asset.

Not all assets are subject to CGT. Common exemptions include the primary residence or family home, granny flats, cars and motorcycles, personal use assets such as boats, furniture, household items, or loans to family and friends. Many types of lump sum payments are also not subject to CGT, and business sales may also be exempt depending on the circumstances.

Most property is subject to CGT, including land, commercial premises, rental properties, holiday houses, and hobby farms. CGT also applies to shares, investments, cryptocurrency, many collectables, foreign currency, and intangible assets.

There are special rules for some specific situations, for example, inheriting assets, relationship breakdown, foreign residents, insurance, or compensation payments.

How is the Tax Calculated?

Tax is calculated on the net gain of an asset sale. Tax is payable on the difference between the purchase price and sale price, less any discount allowed.

The type of CGT event affects how and when capital gains tax is calculated. For example, if an asset is destroyed in an accident, the CGT event occurs when the insurance payout is received.

Good record keeping is key to working out capital gains tax accurately. Ensure you keep all documents related to; asset purchases, including contracts, expenses valuations, and disposal.

CGT is calculated when completing your individual, business, or self-managed super fund tax return and is included in the income tax assessment.

Talk to us to ensure you’re claiming all you’re entitled to and not paying more tax than you should. We’ll make sure you’re receiving any exemptions, discounts, or small business concessions allowed.

For more on our ‘Understanding the Basics’ series, see: